The prolonged COVID-19 pandemic has continued to have a strong impact across the real estate industry, from construction and brokerage operations to the marketing of listings and property closings. That uncertainty presents special challenges in working with existing tenants of leased space.

Building management professionals and tenants themselves have stepped up to outfit properties to support the safety, comfort and overall well-being of their occupants, whether they are workers, customers or short-term visitors.

Today, a strategic focus on retaining tenants and attracting new ones is paramount. In a nationwide survey of 450 building managers and real estate consultants conducted in the summer of 2021 by Blue Skyre IBE and market research company HarrisX, a whopping 94% said their properties have either already or were in the process of upgrading HVAC filtration systems. Two-thirds of buildings have hand sanitation stations and frequent cleaning of high-touch areas, and 62% of those surveyed say temperature checks were required to enter the office.

A full 60% of property managers reported having a documented contingency plan for dealing with COVID-19 surges and 30% were preparing one.

Renegotiating lease terms

As tenants review their long-term space needs and seek changes to their real estate footprint, flexibility has become the norm. With in-office head counts expected to be reduced for the foreseeable future, it’s important to stay open to renegotiating lease terms early to satisfy tenants who might otherwise look to cut and run. The option to sublet their existing space, even for a limited period, has become appealing, especially for tenants unsure of their longer-term space needs.

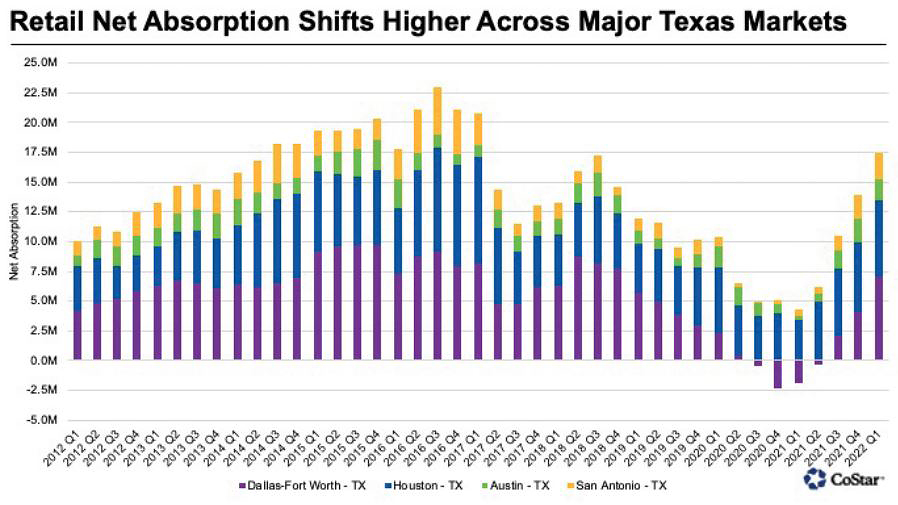

Existing office tenants with traditional three- to five-year leases are having a much easier time shortening those commitments than they have in the past. In the retail sector, investors have reason for optimism. Net new-store openings exceeded closings in the fourth quarter of 2021, and leasing is showing signs of improvement.

Sale-leaseback option

Another option gaining traction is the sale-leaseback. A struggling business can improve its cash position by selling its owned real estate while retaining the right to use the property through a long-term lease. Investors seeking quality, income-producing property with a tenant willing to sign a long-term lease may find this an attractive opportunity. These commitments are usually 10 to 15 years.

What’s influencing office and retail recovery

The principal factors needed for office and retail recovery fall into three main areas:

Striking a balance between owner and tenant needs: Property owners are currently focused on tenant retention at all costs, but they also must satisfy investors.

Offering plentiful amenities and concessions: Owners and building managers will continue to be generous with concessions and keep rent hikes minimal in the next few years, until tenant demand notably increases. On-demand concierge and delivery services that sprang up in the pandemic are likely here to stay.

Remaining patient: Organic business growth may not be sufficient to generate absorption for current vacancies. In the absence of major industry shifts or a new industry entering a local market, population growth will be necessary to absorb the oversupply and bring down vacancy rates, especially in large urban centers.

Digital adoption accelerated by the pandemic has had enormous consequences for work life, consumer habits and the spaces people occupy. And attention to a building’s carbon footprint has become an essential component of any real estate footprint conversation.

Health and safety protocols pertaining to a structure, whether a new build or a retrofit, now double down on concerns like air filtration, insulation and other many other energy-efficiency priorities. Higher green building standards are not only good for the environment, they’ve become essential for business. The investor community’s expectations are changing along with the public when it comes to sustainable practices that will continue to matter long after the pandemic has subsided.

Looking for ways to adapt?

Wipfli can help you navigate real estate decisions during a time of dramatic market and economic volatility. Our advisors help guide your strategic planning and assess trends that matter most to your business. Making smart investment decisions requires thoughtful, proactive planning, not reactive changes in response to immediate events. We’re here to help you and your investors stay on track for the long run. Learn how we help.

Cory Bultinck is a partner in the Minneapolis office of Wipfli. You can reach him at cbultinck@wipfli.com.